.png)

.png)

Insights

·

Jul 14, 2026

·

Taking the MISO cost method beyond the MISO footprint

Optioneer automates nationwide transmission cost estimates.

Read article

CATO Blog Series

Three articles on Britain's competitive transmission experiment: what brought it here, what the world has learned, and what will determine whether it delivers

Article 2 of 3

The UK is not the first country to experiment with competition in transmission infrastructure. A decade of evidence from the US, Australia, and further afield offers some instructive lessons - and a few cautionary tales - for what happens when competitive procurement theory meets delivery reality.

The theoretical case for competition in transmission infrastructure is consistent across every market that has tried it: competitive pressure should drive down costs, encourage innovation, and improve delivery efficiency compared to a guaranteed cost-of-service model. The practical reality has been more nuanced. Competition in transmission works when it is well-designed, consistently run, and applied to the right types of projects. Where those conditions are met, the evidence is genuinely encouraging. Where they are not, competition adds process without delivering the efficiency gains that justified introducing it.

The question for CATO is which of those outcomes Great Britain is heading towards. The honest answer is that it depends substantially on the quality of the planning and analytical work that underpins each tender - and on whether the organisations participating, including the incumbent TOs, invest in the capability to do that work well.

The most ambitious attempt to introduce competition into US transmission came with FERC Order 1000, issued in 2011. Order 1000 required regional transmission planning processes to open up to non-incumbent developers and ended the incumbents' federal right of first refusal on regionally identified projects. In principle, this created conditions for competitive procurement. In practice, a decade later, MIT CEEPR's assessment was direct: while the orders opened up planning processes to non-incumbents and ended the federal right of first refusal, diffusion of transparent, head-to-head competitive procurement programmes was slow.

The US system is fragmented across dozens of states, multiple independent system operators, and competing layers of state and federal jurisdiction. Several states responded to Order 1000 by passing Right of First Refusal (ROFR) laws that effectively re-insulated incumbents from competition at the state level. Some regions developed functional competitive solicitation processes; others found procedural ways to limit them.

The US experience is a reminder that a mandate for competition is not the same as a functioning competitive market. The structural advantages of incumbents - regulatory relationships, existing land access, established supply chains, institutional knowledge - do not disappear simply because the rules require competitive bids.

That said, a cohort of independent transmission developers has emerged in the US that would not otherwise exist. Projects like the Champlain Hudson Power Express, bringing Canadian hydropower underground to New York, and the SunZia line, exporting New Mexico wind energy, represent what independent development can unlock: novel routing decisions, financing structures, and delivery approaches that incumbent utilities rarely pursue on their own. These projects are the exception rather than the rule, but they demonstrate what the best competitive outcomes look like.

Where the US competitive transmission market has matured, the organisations winning bids are not necessarily the largest or most experienced. They are the ones with the most rigorous pre-bid analytical processes. In a competitive framework, the developer who has done the most thorough routing analysis, most credible environmental screening, and most defensible cost modelling will price risk more accurately - and therefore bid more competitively - than one relying on conservative desktop estimates and wide contingency bands.

This is precisely the dynamic playing out in the most competitive US regional markets. Grid United, the independent transmission developer, has adopted Optioneer as its preferred tool for exploring new market opportunities - using it to rapidly assess routing alternatives and constraint profiles across multi-State transmission projects before committing to a bid position. In the PJM solicitation process, Dominion Energy - a major incumbent utility - has deployed Optioneer as part of its competitive transmission development capability, with results that speak to exactly this dynamic.

"This was a really fun assignment. Think about the future: no guardrails, no rationality, just try to be far out there. I took our implementation of an AI routing tool by Continuum Industries and thought about how the past leads to the present and how the future may look using a tool like this. Above all, I believe super tools, like AI for routing, leads to us leaning into our human intelligence. The speed at which we can crunch data allows the human element to become more present in our work. AI = more human = more creativity."

Greg Mathe, Director, Electric Transmission Engagement, Permitting & Land at Dominion Energy

That observation from Dominion is worth sitting with. The argument for tools like Optioneer in a competitive transmission context is not that they replace the judgement of experienced engineers and planners. It is that they compress the data-processing work that currently consumes most of the time available for early-stage planning - freeing the human expertise in the room to focus on the decisions that actually determine whether a project succeeds or fails. In a competitive bid environment, where the timeline from project scope to submission is fixed, that compression is the difference between a bid grounded in rigorous analysis and one built on assumptions.

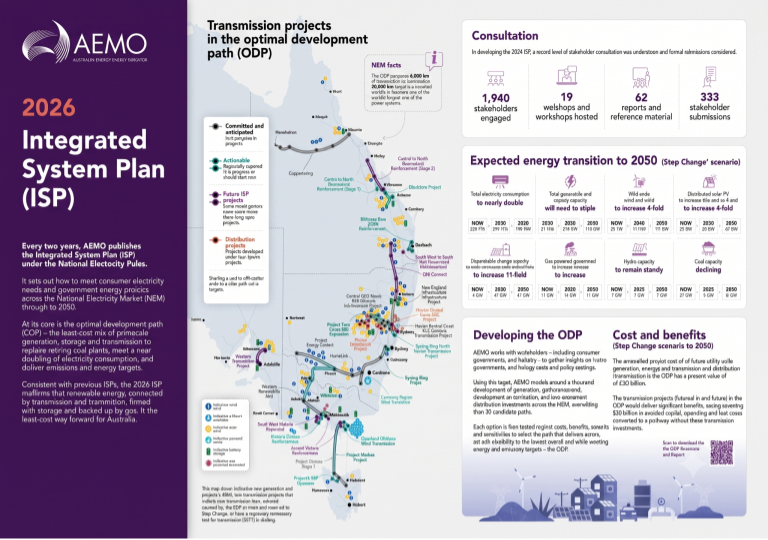

Australia's experience with competitive transmission procurement is more directly relevant to CATO than the US. The Australian Energy Market Operator's Integrated System Plan identifies a pipeline of priority transmission projects, and the framework for delivering them has been designed to allow competition for defined, separable assets - particularly those connecting new Renewable Energy Zones to the main grid.

The REZ infrastructure framework in New South Wales is worth examining. Transmission connecting renewable generation clusters to the grid has been tendered competitively, with developers bidding to build and own assets on regulated terms. The model draws on similar principles to CATO: separable assets, long-term availability-based revenues, early-competition appointment. The Australian experience has confirmed that the hardest problems sit at the boundaries - managing interfaces between competitive and regulated assets, and ensuring that the planning information on which bids are based is detailed and reliable enough to price risk accurately.

Australia has also seen what happens when planning information is poor at the bid stage: risk premiums inflate, bidder counts thin, and the theoretical cost savings of competition erode. The lesson is not that competition is the wrong model. It is that the quality of planning underpinning the tender is as important as the competitive mechanism itself.

For the longest-running evidence on competitive transmission procurement, it is worth looking to Brazil and India. Brazil has run competitive tenders for transmission concessions for over two decades. India's Tariff Based Competitive Bidding framework has channelled substantial private capital into inter-state transmission infrastructure since the late 2000s.

Both markets share a well-documented pattern: early tenders carry higher risk premiums and attract smaller bidder pools; as the market matures and investors develop track records, bid competitiveness increases and consumer costs fall. The Brazilian and Indian transmission markets are now genuinely deep competitive markets. They did not start that way. They became so through consistent programme execution, reliable planning information, and institutional trust-building over many tender rounds.

The implication for CATO is uncomfortable but important: the cost savings that justify the programme are not available immediately. They accumulate over a pipeline of competitive tender rounds. The first few tenders are as much about market-building as about efficiency gains. They need to go well - not just in terms of bid prices, but in terms of actual project delivery - to build the confidence that attracts the breadth of competition that makes the model work over time.

Looking across international competitive transmission markets, the distinguishing factors between programmes that delivered and those that disappointed are consistent:

The OFTO regime's savings of 19 to 23 per cent against regulated counterfactuals are real, but they come from a late-competition model where the asset already exists at tender. Early-competition regimes like CATO, where delivery risk sits with the appointed entity from the design stage, have a different risk profile. The international evidence suggests they can work. It also suggests they are harder to get right - and that the quality of the planning underpinning each project is the variable that most consistently determines whether they do.

Despite these cautions, there is one aspect of the UK's institutional architecture that genuinely distinguishes it from the US experience and provides grounds for measured optimism. NESO operates as a single, nationally accountable system operator responsible both for network planning and for running competitive tender processes. In the US, the fragmentation of planning responsibility across ISOs and state PUCs has been a persistent obstacle to competitive transmission procurement. The UK's cleaner structure, reinforced now by the formal regulatory performance obligation on NESO to advance CATO delivery under Expectation A.4, removes one of the most common failure modes seen elsewhere.

Whether NESO can use that structural advantage to deliver a consistent, credible, and efficient tender programme is the central question of the next three to five years.

In Article 3, we look at what a functioning CATO market actually demands from those who want to win in it - and why the question of delivery against milestones will define whether competition fulfils its promise or becomes another layer of process.

________________

About this series

This three-part series was published by Continuum Industries on 12 March 2026, the day NESO launched its CATO Market Sounding Expression of Interest. Article 1 covers the history of the UK grid and the CATO policy journey. Article 2 examines competitive transmission evidence from the US, Australia, and emerging markets. Article 3 addresses what competitive delivery actually demands in practice, and where the programme will be won or lost.

.png)